January 2023: European hotel industry marked by significant disparities

Although Europe is facing a difficult context with unprecedented inflation rates and political conflicts, tourists are maintaining their holidays on the continent but the situation now reveals disparities between destinations. While Southern Europe is performing well, Northern Europe is once again facing declining results.

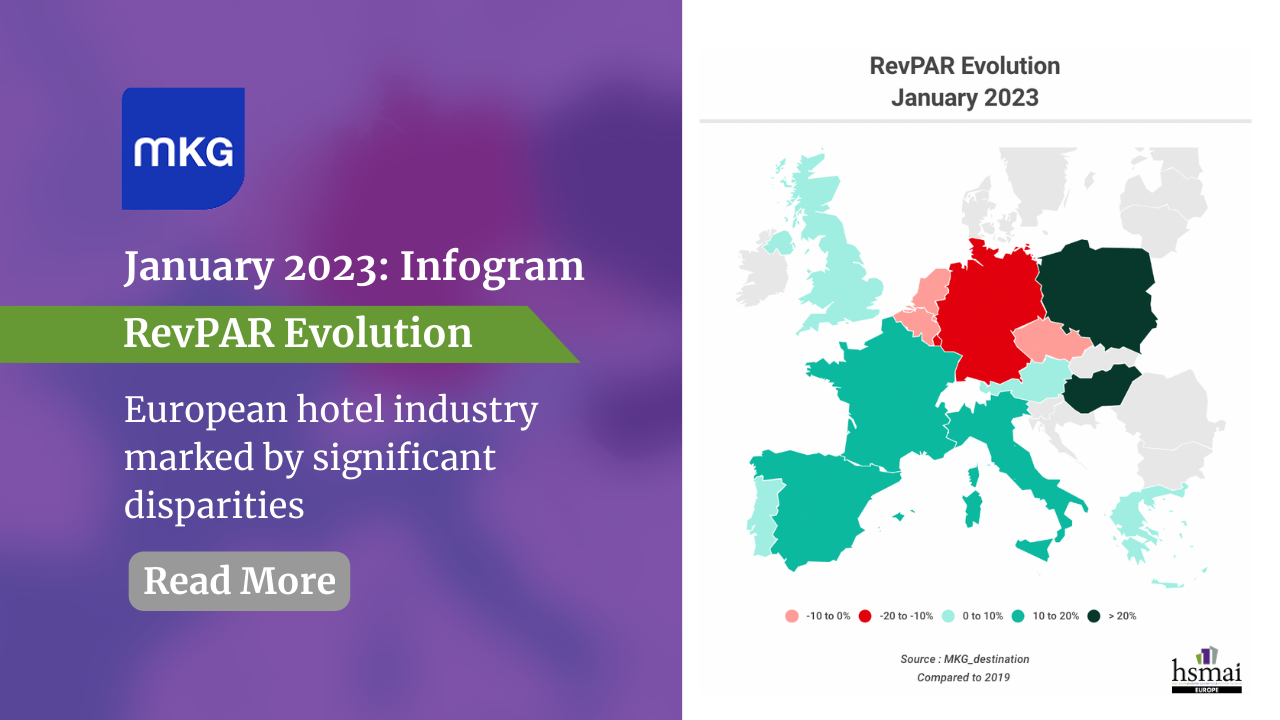

Overall, the European hotel industry posted a higher RevPAR in January than before the crisis, with growth of +3.8%, a positive result but less significant than December’s performance, which showed a gap of +13% compared to December 2019.

For several months now, the dynamic has continued to be driven by an ADR that has risen by +13.3% relative to January 2019. The occupancy rate, on the other hand, is still in deficit compared to the pre-covid period, with a 4.8 point gap.

At the beginning of 2023, it is the budget segment that is performing well with a RevPAR up by +9.3, followed by the economy (+5.3%), the upscale one (+3.2) and finally the midscale (+2.5%). The upscale market managed to increase its ADR by +18.8%, while the midscale one saw a more “moderate” increase (+11.5%). Occupancy rates, on the other hand, are lagging further behind on the upscale market (-7.7 points vs. January 2019) while budget hotels are only -2.4 points away from pre-crisis levels.

More locally, Hungary continues to show an irrational increase in activity: +68.5% RevPAR growth explained by the 81.3% increase in ADR skewed by the serious inflation rate in January (+25.7%).

In addition to this phenomenon biased by the particular economic situation, Poland is on the podium on a European scale with a +24.8% increase in its hotel activity in December due to its ADR which took +31%.

The rest of Southern Europe is also doing rather well: the hotel performances of Spain (+11.2%), Greece (+9.7%) and Portugal (8.1%) are also driven by considerably higher ADR (between 12 and 21%). However, the delay in terms of occupation is more marked in Portugal (-6 points) than in the other two countries (-2.6 points in Spain and -1.1 points in Greece).

Less ahead in terms of RevPAR, the UK and Austria remain better performing than in January 2019 with increases of +6.9% and +3.4% respectively.

On the other hand, some countries show completely opposite dynamics. Both the Benelux countries and Germany are back in the red this month, whereas the results were encouraging at the end of 2022. While Belgium and the Netherlands are behind by only 5.2% and 5.3%, Germany has seen its RevPAR fall by -22.1% compared to January 2019. Luxembourg is down -16.7%. Will these business-dominated countries manage to recover as the school holidays approach next month?

{kind=link}